Celulosa Argentina S.A.’s U$S3,699,506 Class 20 Notes and U$S11,300,494 Class 21 Notes Offering

![]()

Counsel to Celulosa Argentina S.A. in the issuance of 8.00% Class 20 Notes for U$S3,699,506 due February 8, 2026 Class 20 Notes are denominated and payable in U.S. dollars and 7.00% Class 21 Notes for U$S11,300,494 due February 8, 2026 Class 21 Notes are denominated in U.S. dollars and payables in Pesos, both under its U$S 150,000,000 Global Notes Program.

Banco de Servicios y Transacciones S.A., Puente Hnos. S.A., Balanz Capital Valores S.A.U., Zofingen Securities S.A., Invertironline S.A.U, Banco Supervielle S.A., Facimex Valores S.A., and GMC Valores S.A. acted as placement agents of the Notes. Banco de Servicios y Transacciones S.A. and Puente Hnos. S.A. acted as arrangers of the issuance, and Banco de Servicios y Transacciones S.A. also acted as settlement agent of this issuance.

Regulation of Foundations Law: Government reorganization and Sale of state-owned companies

On August 5, 2024, the Government released Decree 695/2024 (the “Decree 695”) that regulates Title II “State Reform” of Law 27,742 “Foundations Law” (“Ley de Bases y Puntos de Partida para la Libertad de los Argentinos”).

A summary of the most relevant aspects on the regulations related to Government reorganization and Sale of state-owned companies are described below. Additional comments to the Foundations Law on these subjects are also available here and here.

1. Government reorganization

The Ministry of Economy shall propose to the National Executive Power the modification, transformation, unification, liquidation or dissolution of public trust funds in accordance with Section 5 a), b) and c) of Law 27,742 and other applicable provisions.

In addition, Decree 695 empowers the Ministry of Economy to issue complementary regulations to implement this procedure.

2. Sale of state-owned companies

2.1. Report

For the purposes of obtaining the National Executive Power’s authorization to proceed with the sale of state-owned companies, the Ministry or Secretary in control of the respective state-owned company (list that includes ENARSA, AYSA, Belgrano Cargas, Intercargo, Corredores Viales, among others) must submit to the National Executive Power a detailed report with a specific proposal of the most adequate procedure and modality for the sale of such any state owned company (the “Report”), after the intervention of the Agency for the Transformation of State-Owned Companies (Agencia de Transformación de Empresas del Estado).

2.2. Call for bids

Call for bids shall be published for, at least, seven (7) days, and the last publications shall be made, at least, thirty (30) days prior to the deadline for the submission of bids, according to the complexity of the procedure. Additionally, the call for bids must be published on the website of the enforcement authority responsible for the procedure.

For international call for bids, the call also must be published in at least one website that allows adequate access to foreign interested parties, for a term of three (3) days, at least forty-five (45) calendar days prior to the deadline for the submission of bids. The enforcement authority may also issue invitations to participate to all those human or legal persons, with national or foreign capital, that considers convenient.

2.3. Liquidation

In the case of sale of the above mentioned companies when the transfer of contracts under execution to the provinces is required, the Report shall also detail the amounts involved in any such contract, as well as any related agreements.

The company in liquidation, in cooperation with the Agency for the Administration of State Assets (Agencia de Administración de Bienes del Estado) must elaborate an inventory of its assets, including their valuation. If applicable, a priority order for the sale of the assets must be defined.

2.4. Other provisions

Prior to the closing of contracts, the Office of the Attorney General (Procuración del Tesoro de la Nación) and the Agency for the Transformation of State-Owned Companies may make observations and/or suggestions. In that event, the enforcement authority shall perform the referred modifications, and submit a final report to the National Executive Power for its approval. Once the procedure is completed, the enforcement authority shall draft a final report to the General Auditor Office.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Legal Advice in Petrolera Aconcagua Energía S.A.’s Class XII Note Issuance

Counsel in the issuance of Petrolera Aconcagua Energía S.A.’s 2.00% Class XII Notes, for US$ 25,023,948 issued on July 18, 2024, and due July 18, 2026, under its US$ 500,000,000 Global Notes Program.

Banco de Servicios y Transacciones S.A., acted as arranger and placement agent, and Banco Mariva S.A., Banco Supervielle S.A., Banco Santander Argentina S.A., Banco de Galicia y Buenos Aires S.A.U., SBS Trading S.A., Consultatio Investments S.A., Allaria S.A., Adcap Securities Argentina S.A., Facimex Valores S.A., Balanz Capital Valores S.A.U. and Invertir en Bolsa S.A., acted as placement agents.

Legal Advice in the Issuance of Series XIV Notes of MSU S.A. for US$ 33,500,000

Counsel to Banco de Galicia y Buenos Aires S.A.U. as arranger, placement agent and settlement agent, and Balanz Capital Valores S.A.U., Banco Santander Argentina S.A., Banco de Servicios y Transacciones S.A., Puente Hnos. S.A., Banco de la Ciudad de Buenos Aires, and Adcap Securities Argentina S.A. as placement agents, in the issuance of MSU S.A. 7.50% Series XIV Notes for US$ 33,500,000 issued on July 23, 2024, and due July 23, 2027, under its US$ 200,000,000 Global Notes Program.

Banco de Galicia y Buenos Aires S.A.U. acted as arranger, placement agent and settlement agent, and Balanz Capital Valores S.A.U., Banco Santander Argentina S.A., Banco de Servicios y Transacciones S.A., Puente Hnos. S.A., Banco de la Ciudad de Buenos Aires, and Adcap Securities Argentina S.A. acted as placement agents.

Foundations Law: Labor Reform

1. Promotion of registered employment

Employers may regularize, within 90 days as of the regulation of the Foundations Law, the labor relations that are not registered or were registered in a deficient or partial manner (lower remuneration or date of entry after the real one).

The regulation of the law will precisely define the effects of this regularization, which in principle would include: (i) the extinction of the criminal action in process and the remission of fines for infractions; (ii) the removal of the employer from the registry with labor sanctions (“REPSAL”); (iii) the remission of debts of withholdings and contributions (except health care regime) in no less than 70% of the total; including those that are in dispute in a court of law.

Workers whose contracts have been regularized within the framework of the law and its regulations, will be entitled to compute, only for the purposes of the payment of the Universal Basic Benefit ("PBU") and for Unemployment Benefit, up to 60 months of services with contributions, calculated on the amount of the minimum, vital and mobile salary.

2. Labor modernization

Under this heading, the Foundations Law produces a very significant labor reform over the Employment Contract Act (“ECA”) and other labor regulations; the most important guidelines of which are as follows:

2.1. Repeal of fines for irregular registration

The Foundations Law eliminates all provisions of the National Employment Law No. 24,013 which set fines for lack of registration or deficient registration of the employment relationship. Law No. 25,323, which imposed fines for irregular registration (Section 1) and for failure to pay severance payments for dismissal without cause (Section 2) are also repealed by the Foundations Law.

2.2. Elimination of fines for failure to deliver work certificates

Through the repeal of Sections 43 to 48 of Law No. 25,345, the fines related to the failure to deliver the certificates of services and remunerations (Section 80 ECA) and for failure to pay the contributions withheld from the worker (Section 132 bis ECA) are eliminated.

2.3. Registration of the employment contract

There will be a new mechanism for the registration of the employment relationship, to be defined by the regulations, which will be simple and electronic. There will also be a simple mechanism for the issuance of salary slips and a unified contribution will be provided for companies with up to 12 workers.

2.4. Contractors and intermediaries

The law sets out the validity of the registration made by the original employer in relationships with contractors and staffing agencies. In the same sense, due to the amendment of Section 29 of the ECA, it is established that workers hired by third parties to be assigned to companies will be considered direct employees of the company which register the relationship, thus eliminating the risk of irregular registration of workers assigned to companies by third party contractors.

2.5. Deficient Registration

The worker may denounce the lack or partial registration of the employment relationship before the AFIP, through the electronic means that the authority will offer for such purposes. If such deficiency is established by the Court, the Judge will report the AFIP, which will determine the relevant social security debts. The corresponding debt will consider the contributions paid by the independent contractor.

2.6. Scope of application of the ECA

Service and agency contracts (among others) regulated by the National Civil and Commercial Code are excluded from the scope of application of the ECA.

2.7. Presumption of employment contract. Civil contracts

Professional services or trades that foreseen the issuance of official invoices by the provider do not fall under the presumption of the existence of an employment contract when the services are rendered by individuals. This understanding extends its effect to Social Security obligations.

2.8. Trial period

The trial period (Section 92 bis ECA) is of 6 months. This period may be extended by collective agreements to 8 months in companies with 6 to 100 workers, and up to 12 months in companies with a payroll of no more than 5 workers. These provisions will also apply to the national agricultural labor regime.

2.9. Pregnancy protection

The prohibition for pregnant women to work during the 45 days before and after childbirth is maintained, although as a result of the reform the employee is granted the option to reduce the pre-birth leave to 10 days, accumulating the remaining period to the postpartum period.

2.10. Just cause for dismissal

The law amends Section 242 of the ECA, expressly including as causes for dismissal, the following: (i) active participation in blockades or takeovers of the establishment; (ii) when as a result of the participation in strikes, (a) the freedom to work of those who do not participate in the strike is affected; (b) the entry of persons or things to the establishment is obstructed; (c) damage is caused to persons or assets of the company or third parties. Before dismissal because of these non-compliances, the employer must formally request the worker to abandon his attitude. This request is not necessary in the case of damage to persons or things.

2.11. Special compensation for discriminatory dismissal

Judges may increase the severance compensation between 50% and 100% (depending on the seriousness of the discriminatory act) in cases where the employee proves before Court that his/her dismissal was motivated by reasons of ethnicity, race, nationality, sex, gender identity, sexual orientation, religion, ideology or political or union opinion. Despite the discrimination scenario, the employee will not have the right to claim reinstatement.

2.12. Severance fund

Within the framework of a collective bargaining agreement, the parties may replace the current severance payment scheme with a "severance fund ". Its characteristics will be defined by the regulations. On the other hand, employers may choose to contract a private capitalization system (or self-insure) to cover the cost of the severance indemnification provided by the ECA or for the payment of a bonus agreed within the framework of mutual termination agreement.

2.13. Independent worker with collaborators

The Foundations Law incorporates a new category of self-employed workers, providing that an autonomous worker may work with up to 3 self-employed workers to carry out a productive undertaking, under a special regime to be regulated by the National Executive Power. There will be no employment relationship between those parties, unless in the reality of the relationship the notes of subordination that characterize any relationship of dependency are visualized. Anyway, as per the conditions to be defined by regulations, these workers will be included under the Social Security regimen, Health Care, and the Labor Hazards Law.

***

For additional information, please contact Federico Basile.

Law on Palliative and Relevant Tax Measures

On June 28th, 2024, the National Chamber of Deputies finally passed the Law on "Palliative and Relevant Tax Measures" (the "Tax Measures"), rejecting the amendments introduced by the National Senate on Income Tax (for employees) and Personal Assets Tax.

Below, we summarize the most relevant aspects of the Tax Measures:

Exceptional Regularization Regime for Tax, Customs, and Social Security Obligations (“moratorium”)

- Included obligations: the moratorium applies to tax, customs, and social security obligations (with some exclusions) due by March 31, 2024, inclusive, and for infringements committed up to that date, whether related to those obligations or not.

- Compensatory and punitive interests forgiveness: the moratorium establishes the following scheme for interests forgiveness: a) 70% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments, and the adherence to the moratorium takes place within the first 30 calendar days from the issuance of the regulation by the Tax Authorities (hereinafter, the “AFIP”, as per its acronym in Spanish); b) 60% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 31st to the 60th calendar day; c) 50% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 61st calendar day to the 90th calendar day; d) 40% of forgiveness if total debt is regularized through a payment plan and the adherence to the moratorium takes place within the first 90 calendar days; e) 20% of forgiveness if the total debt is regularized through a payment plan and the adherence to the moratorium takes place after the 91st calendar day.

- Financing: for cases d) and e) mentioned above, it is established that: (i) individuals must make a prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 60 monthly installments; (ii) Micro and Small Enterprises must make a prepayment of 15% of the debt and they are allowed to pay the remaining amount in up to 84 monthly installments; (iii) Medium Enterprises must make prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 48 monthly installments; (iv) other taxpayers must make a prepayment of 25% of the debt and they are allowed to pay the remaining amount in up to 36 monthly installments. In all cases, future regulations will set a financing interest, which will be calculated according to the rate established by the Banco de la Nación Argentina for commercial discounts.

- Other benefits: the adherence to moratorium implies the forgiveness of 100% of fines and the extinction of criminal actions.

Asset Regularization Regime (“Tax amnesty”)

- Subjects: (i) individuals, undivided estates, and companies that, as of December 31th, 2023, are deemed Argentine tax residents, whether or not they are registered as taxpayers before AFIP; (ii) individuals who were Argentine tax residents before December 31th, 2023, but have lost such status by that date. If latter adhere to the Tax amnesty, they will be deemed Argentine residents as of January 1st, 2024.

- Adherence period: the referred subjects can adhere to the Tax amnesty up to April 30th, 2025. The National Executive Branch may extend this period until July 31st, 2025.

- Included Assets: assets located in the country and abroad, including national and foreign currency, movable and immovable property, securities and shares, credits and rights, cryptocurrencies (only as assets in the country) owned, possessed, hold, or custodied by the taxpayer as of December 31st, 2023.

- Special tax: the special tax rate will be 5%, 10%, or 15%, depending on the moment in which the tax return is filed, and the payment is made.

- Amnesty without special tax: subjects will be able to regularize up to USD 100,000 without any penalty. If the amount subject to amnesty exceeds USD 100,000, no penalty will apply if the funds remain in a special account until December 31st, 2025. Amounts deposited in the special account can be invested in certain financial instruments specified by the regulation.

- Benefits: (i) extinction of all civil or criminal actions derived from the non-compliance of obligations related to the regularized assets; (ii) tax and interest forgiveness; (iii) inapplicability of the unjustified wealth increase presumption.

Personal Assets Tax ("PAT")

Special PAT Prepayment Regime: Tax Measures include an optional and voluntary prepayment regime for PAT, which has the following characteristics:

- Subjects: (i) individuals and undivided estates that, as of December 31st, 2023, are deemed Argentine tax residents; (ii) individuals who were Argentine tax residents before December 31st, 2023, but lost such status by that date. If they adhere to this Regime, they will be deemed Argentine tax residents again.

- Adherence period: subject will be able to adhere to this regime up to July 31st, 2024. This period may be extended up to September 30th, 2024.

- Included tax periods: 2023 to 2027 (unified) or 2024 to 2027 (unified) in case of taxpayers that have adhered to the Tax amnesty.

- Calculation method: PAT tax base is determined by considering the taxpayer's assets as of December 31st, 2023 -with certain particularities- multiplied by 5.

- Tax rates: the following rates are applied: (i) individuals and undivided estates: 0.45%; (ii) taxpayers who have regularized assets under the Tax amnesty: 0.50%. Since tax period 2028, maximum tax rate will be 0,25%

- Initial payment: taxpayers adhered to this regime must make an initial prepayment of -at least- 75% of the total PAT determined according to the regime's rules.

- Benefits: (i) exclusion from the payment of PAT and any other wealth tax for the tax periods 2023 to 2027 (or 2024 to 2027, as the case may be); and (ii) tax stability on those taxes up to 2038.

PAT Law:

- Certain modifications are established for the tax period 2023.

- The PAT non-taxable minimum is modified: ARS 100,000,000 (or ARS 350,000,000 for real estate that qualifies as only residence).

- The Tax measures include the unification of PAT rates for assets located in the country and assets located abroad as follows:

- Tax period 2023: from 0.50% to 1.50%;

- Tax period 2024: from 0.50% to 1.25%;

- Tax period 2025: from 0.50% to 1%;

- Tax period 2026: from 0.50% to 0.75%;

- Tax period 2027: a single rate of 0.25%.

- The Tax measures include benefits for compliant taxpayers:

- To qualify as a compliant taxpayer, the taxpayer (i) must not have regularized assets under the Tax amnesty; and (ii) must have submitted the PAT returns related to tax periods 2020 to 2022, inclusive, in a timely and proper manner, and must have fully paid, before December 31st, 2023, the PAT due to the AFIP resulting from each of those tax returns.

- Compliant taxpayers will have a 0.50% reduction in the PAT rates for tax periods 2023 to 2025.

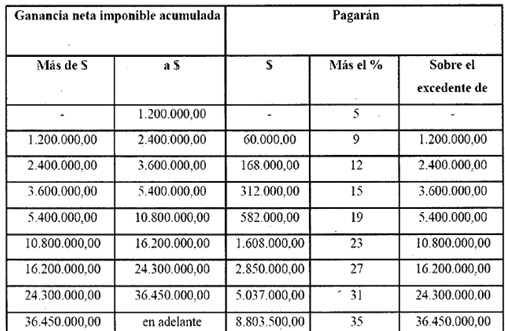

Income Tax ("IT")

- The Tax measures repealed the “cedular IT” previously applied to employees, which established a special and unique deduction equivalent to 180 annual minimum salaries for IT determination.

- In replacement, it is created a new regime to determine employees’ IT.

- This new regime repeals certain exemptions, deductions, and benefits previously applicable to employees.

- Certain personal deductions are reinstated.

- Non-taxable minimums, scales, and personal deduction amounts are updated.

- The following scale is established for employees’ IT determination:

- From 2025, scales will be adjusted for inflation every semester (in January and July of each year) based on the CPI (Consumer Price Index).

- An exceptional adjustment for inflation will take place in September 2024, regarding months June to August. Therefore, the amounts corresponding to the first half of the current year will not be adjusted.

- The National Executive Power is authorized to exceptionally increase deductions during 2024.

-

Other modifications

- The billing caps of the Simplified Regime for Small Taxpayers were updated. The National Executive Power is authorized to increase those caps during 2024.

- The Real Estate Transfer Tax (“ITI”) was repealed.

- A tax transparency regime for consumers was created.

-

***

For additional information, please contact Gastón Miani or Leonel Zanotto.

Foundations Law: Electric Energy

The National Executive Power is entrusted, for a term of one (1) year, to make amends to the electric energy regulatory framework, namely composed by Laws No. 15,336 and No. 24,065, in order to guarantee, among others, free international trade of electric energy; free commercialization and expansion of the electric energy markets; the adjustment of the fees of the energy system based on the real costs of the supply, to cover investment needs and guarantee the continuous and regular provision of public services; and the development of electric energy transportation infrastructure.

Common regulations on electric energy and natural gas chapters

Appeals and objections to sanctions

Acts and sanctions issued by the highest authority of the regulatory body may be challenged without the need to file an appeal, directly before the National Court of Appeals for Federal Administrative Matters.

Unification of regulatory bodies

Foundations law unifies the electricity and gas regulatory bodies under a single entity, the “Ente Regulador del Gas y la Electricidad”.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Sale of state-owned companies

The Foundations Law declares subject to sale the following state-owned companies:

- Energía Argentina S.A.

- Intercargo S.A.U.

- Agua y Saneamientos Argentinos S.A.

- Belgrano Cargas y Logística S.A.

- Sociedad Operadora Ferroviaria S.E. (SOFSE)

- Corredores Viales S.A.

Nucleoeléctrica Argentina Sociedad Anónima (NASA) and Complejo Carbonífero, Ferroviario, Portuario y Energético a cargo de Yacimientos Carboníferos Rio Turbio (YCRT) equity interests will be subject to sale as well, to the extent that the National Government retains a majority stake, and a private ownership (PPP) program for the employees is set up.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Hydrocarbons and Gas

1. Amendments to Law No. 17,319 on Hydrocarbons

1.1. Scope and goals of national policies

The Foundations Law introduces several amendments to Law No. 17,319 including, activities of storage and processing to the already included activities of exploitation, transportation, industrialization, and commercialization of hydrocarbons, empowering the National or provincial Executive Powers to grant permits, concessions, or authorizations for the transportation, storage, or processing of hydrocarbons. It also adds as the main objective of the national hydrocarbon’s regulation the maximization of the income obtained from the exploitation of the resources.

With regards to processing, it extends the obligation concerning the transportation of hydrocarbons to those authorized to process hydrocarbons of third parties, up to five percent (5%) of the capacity of their facilities. It shall not compromise the safety of the process and the applicant will be responsible for the costs related to the connection to the plant. In the case of liquid fuel processing plants, the service must include the storage service. Refining services and its related storage facilities and natural gas liquefaction plants are excluded.

Regarding storage, the addition of section 44 bis determines that the authorizations for underground storage of natural gas enables the storage in natural reservoirs of depleted hydrocarbons.

Authorizations may be granted in areas subject to exploration permits and/or exploitation concessions of its own or from third parties and in areas that are no longer subject to exploration permits and/or exploitation concessions.

Any other underground storage of natural gas will not require authorization. Storage authorizations shall not have a term.

Likewise, the Foundations Law abrogates certain sections of Law No. 17,319 which originally provided for a notorious participation of the National Government as well as the preference for companies of Argentine capital in hydrocarbon activities. Thus, the Law eliminated, among others, Sections 11, 13, 91, 91, 96 and 101.

1.2. Free market

The Foundations Law ratifies the possession of permit holders and concessionaires over the hydrocarbons they extract. They may freely commercialize it according to the regulations, and the National Executive Power shall not fix the prices in the domestic market.

Concerning the export of hydrocarbons, it enables the free international trade of hydrocarbons -in line with the strategic projects export regime of the RIGI- and they may freely export hydrocarbons and/or their derivatives.

1.3. Exploration activities

The Foundations Law abrogates section 15 of Law No. 17,319 which established prior approval from the application authority to recognition works and its scope. .

On the other hand, it modifies section 21 of Law No. 17,319 regarding the payment of royalties for hydrocarbons extracted during exploration, applying the royalty “committed in the award process”.

1.4. Amendments to the award system

Bidding terms and conditions shall contain the conditions and guarantees that offers must comply and the minimum investments amounts to be made by the successful bidder. Likewise, it shall establish mechanisms to adjust royalties according to the total investments made, the income and the operating expenses incurred, among others. The evaluation of offers shall consider these items, as well as the total project value.

On the other hand, the Foundations Law introduces that existing exploitation concessions, at the end of its term, shall not be awarded without a new bidding procedure. This procedure shall be carried out at least one (1) year prior to the expiration of such concessions.

1.5. Investment regime

Investment regime has been limited to the obligation of the concession holder to carry out, within reasonable terms, the necessary investments for the execution of the works required for the development of the area.

1.6. Canons and royalties

The Foundations Law updates the amounts that the holder of an exploration permit must pay annually and a fee for each square kilometer or fraction, establishing a mechanism to facilitate future updates, according to the following scale:

- Basic Term:

- 1st Period: the equivalent amount of zero point fifty (0.50) barrels of oil per square kilometer in pesos.

- 2nd Period: the amount equivalent of two (2) barrels of oil per square kilometer in pesos.

- Extension: the amount equivalent to fifteen (15) barrels of oil per square kilometer in pesos.

Exploitation concessionaires must pay annually the amount equivalent in pesos to ten (10) barrels of oil per square kilometer or fraction thereof covered by the area.

These royalties will be adjusted according to the average price of an oil barrel of the 'ICE Brent First Line'.

Exploitation concessionaires shall pay monthly a royalty to the grantor for the produced and effectively exploited hydrocarbons, based on a percentage equivalent to the one determined in the awarding process.

In addition, the National or the provincial Executive Power may reduce the royalty up to five percent (5%) considering the productivity, conditions, and location of the wells.

Authorizations to storage gas underground mentioned above shall only pay royalties at the time of its first commercialization.

1.7. Exploitation by foreign entities

The Foundations Law overturns Section 51 of Law No. 17,319, which did not allow foreign public legal entities to submit bids.

1.8. Non-Conventional Exploitation and terms of concessions

It also eliminates the obligation of the exploitation concessionaire to request a new concession for non-conventional exploitation, simplifying the process. They must require the subdivision of the area and the conversion from conventional to non-conventional. The request must be based on a pilot plan that, in accordance with technical and financial criteria, is aimed at the commercial exploitation of the discovered reservoir. This request may only be submitted until December 31, 2028. The enforcement authority will decide within sixty (60) days, and once the reconversion request is approved, the term of the reconverted concession will be thirty-five (35) years computed from the date of the request.

1.9. Modifications to transport concessions regulation

The regime of transportation concessions is modified to a regime of authorizations, if the transporter (i) has technical and financial capacity, and (ii) has an address in Argentina. The enforcement authority will keep a registry of those authorized to transport hydrocarbons.

The owners of projects and/or facilities for industrialization processes may request an authorization to transport hydrocarbons and/or their derivatives to their industrialization or commercialization facilities. These authorizations shall not have a term.

In the case of transportation authorizations awarded to explotation concessionaires, the authorized parties may request extensions for a term of ten (10) additional years.

The idle capacity of a gas pipeline must be available to third parties for its use, according to the needs of the authorized party. However, they may not act in unfair competition or abuse of their dominant position in the market.

On the other hand, holders of an underground gas storage authorization may request an authorization to transport hydrocarbons to their storage facilities and from these to the transportation system, which shall also not have a term.

2. Amendments to Law No. 24,076 on Gas Regulations

2.1. Exports and imports

While natural gas imports will continue authorized with no need for prior approval, exports must be regulated by the National Executive Power, considering the new wording of Section 6 of Law No. 17,319.

2.2. License renovation

The additional period of extension of the licenses of public services of transport and distribution of natural gas is extended from ten (10) to twenty (20) years. Considering that the original term of thirty-five (35) years expires in 2027, if the renewal is granted, such licenses would expire in 2047.

2.3. Transporters, distributors, and storage

The Foundations Law keeps the obligation to take the necessary measures to ensure the supply of non-interruptible services, and it is added that these, by themselves or by third parties, may acquire, build, operate, maintain, and manage natural gas storage facilities, according to the limitations established.

2.4. Liquefied Natural Gas (“LNG”)

Together with the provisions set forth for the RIGI (see comment to the RIGI, here), other terms applicable to LNG are included.

According to the Foundations Law, LNG exports must be authorized by the Secretary of Energy, within one hundred and twenty (120) days following the request from the relevant party.

LNG export authorizations will be granted for a term of thirty (30) years as of commissioning of the facility.

It is further clarified that it will not be necessary for the applicant to have LNG purchase and sale contracts in place or the total volume for the purposes of granting the LNG export permit. The granting of an authorization will imply the right to export all the volumes authorized in such capacity continuously and without interruptions, restrictions, or reductions, as well as the right to access without restrictions or interruptions to the supply of natural gas or to the transportation, processing, or storage capacity of any kind.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Amendments to the Public Works Concession Law No. 17,520

Law 17,520 is subject to several amendments, which include the following:

1. Forms of concession and sole purpose vehicles

The National Executive Power may, acting as grantor, award public works, infrastructure concessions and public services for a fixed or variable term to private companies, acting as concessionaires, for the construction, maintenance or operation of public works, infrastructure or public services by charging of fees, tolls, or other payment conditions.

Special purpose vehicles incorporated solely for the purpose of holding the concession is enabled.

2. Private initiatives

Private initiatives are admissible and shall be analyzed by the enforcement authority. In all cases the financing must be private.

3. Requirements of the bidding process and terms of the concession agreement

Material terms of the concession agreement (e.g., term, payment, allocation of responsibilities) shall be clearly defined in the relevant bidding process, which shall also include:

- The terms applicable to each party’s obligations, and the consequences which may arise upon either party falling out of compliance with its obligations.

- The terms of payment, as well as the procedures for revising the contract price to preserve its financial balance.

- The features to adapt the execution forms to technological advances, financing needs and requirements that may arise during its term.

- The power of the national public administration to unilaterally establish variations to the contract only with respect to the execution of the project up to a maximum limit of twenty percent (20%) of the total value of the contract, preserving its financial balance.

- The grounds for termination of the contract due to fulfillment of the object, term-expiration, mutual agreement, default of either party, reasons of public interest or other causes, indicating the applicable procedure, the compensation corresponding to cases of early termination, its scope, method of determination and payment.

- The right to transfer the contract to a third party if such party meets similar requirements as the transferor and that, at least twenty percent (20%) of the original term of the contract or of the committed investment has passed, whichever occurs earlier. The authority of control must issue a legal opinion prior to authorization by the contracting authority.

Prior to any assignment, the consent of the financiers and guarantors must be obtained, as well as the authorization of the concession grantor.

4. Works financing

The Foundations Law includes certain provisions regarding financing of works to enhance the likelihood of third-party financing, including the following:

In case of economic imbalance in the contract due to causes not attributable to its parties, both parties shall be entitled to renegotiate the contract to re-balance it, or otherwise agree on its termination by mutual consent.

At the time of making its offers, bidders shall indicate the economic-financial equation, explaining the Current Net Value and/or the Internal Rate of Return (IRR).

In the event of force majeure or acts by the Government that cause an alteration of such equation, the term of the concession may be extended. Likewise, in the event of force majeure, the grantor must guarantee the minimum income that may be agreed in the contract.

5. Termination

In the event of termination of the concession contract by the grantor for convenience, limitation of liability laws (e.g., State liability law) shall not be applicable.

The grantor’s decision to terminate the contract by convenience must be duly founded, indicating:

-

- the impartial technical reports that justify the termination of the contract;

- the causes and the reasons that support a different evaluation of the public interest;

- the submission of the determination of the scope of the concessionaire's compensation to the consideration of the technical panel and/or the arbitration tribunal acting within the framework of the contract, in those cases in which the concession contract does not contemplate formulas or other mechanisms for its determination; and

- the term of payment of the compensation.

6. Dispute settlement mechanisms

All concession contracts must consider as dispute prevention and settlement mechanisms resolution, conciliation, and arbitration mechanisms to resolve technical or economic disputes between the parties. If matters are not settled through these mechanisms, they may also submit them to a Technical Panel or solve them through Arbitration.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.