Foundations Law: Hydrocarbons and Natural Gas Regulation

On November 29, 2024, the Government of Argentina released Decree 1057/2024 (“Decree 1057”), that regulates Chapters I, II, and VI of Title VI of Law No. 27,742 ( “Foundations Law”), which modifies Law No. 17,319 on Hydrocarbons (“Hydrocarbons Law”), Law No. 24,076 on Natural Gas (“Natural Gas Law”), and environmental legislation under Law No. 27,007 (the "Environmental Regulation").

To review our comments on the Foundations Law, please access here.

The key takeaways of Decree 1057 are summarized below:

1. Regulation of the Hydrocarbons Law

- Decree 1057 establishes certain guidelines regarding the activities of exploration, exploitation, processing, transportation, storage, industrialization, and commercialization of hydrocarbons, including:

- Free market principles;

- Competitive markets through the participation of the actors across the production chain and related sectors;

- Local price alignment with international market conditions, ensuring hydrocarbons supply and parity in imports and exports;

- Efficient resource allocation;

- Long-term contracts, competitiveness, productivity, and integration into global trade; and

- Ensuring present and future hydrocarbons local supply.

- Interested parties in developing the previously mentioned activities shall (i) establish a legal address in Argentina and (ii) demonstrate financial and technical capacity. Regarding interjurisdictional and international transportation, the Government shall grant concessions and authorizations for inter-provincial operations, as well as for imports and exports.

- Decree 1057 provides for the free exports of hydrocarbons, subject to specific requirements, that include the submission to the Secretary of Energy of documentation that evidences (i) the details of the planned operation, (ii) production capacity, (iii) commercial agreements, (iv) compliance with the destination country requirements, (v) legal representative information, (vi) semi-annual and annual projections of volume and quality of hydrocarbons, port of in operation, and loading estimated date. The Secretary of Energy may object exports in case of:

- Shortages affecting local supply;

- Inaccuracies in the submitted documentation;

- Evidence of anti-competitive practices; and

- Unforeseeable variations of prices in the local market.

- The Secretary of Energy shall manage an export registry to monitor approved, objected, and completed transactions, and shall issue the Free Export Certificate in favor of the interested party i if no objections are raised.

- The Secretary of Energy may consider the export of surplus volumes of gas.

- Concessionaries shall submit annually the information regarding the availability of the resources and estimated production.

2. Natural Gas Law Regulation

- Decree 1057 provides for the free exports and imports of Liquified Natural Gas (“LNG”). The Secretary of Energy shall regulate its procedure, contemplating its impact on the current and new infrastructure and its investment amounts. Interested parties shall submit documentation that evidence (i) availability of resources; (ii) technical and financial capacity; (iii) LNG maximum volumes to be exported; and (iv) if the project has filed for the Large Investments Incentive Regime (“RIGI”).

- The Secretary of Energy will elaborate a Declaration on the Availability of Gas Resources, which must be updated at least every five (5) years, including market conditions, estimated production and exports amounts, and its impact on the local demand.

- The Secretary of Energy may object LNG exports in case of (i) shortages affecting local supply; (ii) lack of capacity to export LNG; (iii) inaccuracies in the submitted documentation; and (iv) evidence of anti-competitive practices. If no objections are raised, the Secretary of Energy shall issue a Free Export Authorization.

- Transportation and distribution licenses are eligible for a twenty (20) year extension beyond the initial thirty-five (35) year term, subject to compliance with obligations and corrections of deficiencies identified by the National Gas Regulatory Body (“ENARGAS”).

3. Environmental Regulation

In order to promote a consolidated environmental regulation, Decree 1057 instructs the Secretary of Energy to identify a coordinated procedure to amend the legal framework, considering, among others: (i) environmental licensing processes, (ii) abandonment of wells and installations, (iii) management of environmental liabilities, waste, emissions, and effluent management, (iv) safety conditions, (v) greenhouse gas emissions and decarbonization, (vi) guarantees and insurance for environmental contingencies, (vii) participation and access to public information, (viii) corporate environmental and social responsibility, (ix) inspections and sanctions.

***

For additional information, please contact Nicolás Eliaschev, Javier Constanzó, Daiana Perrone, Milagros Piñeiro, Victoria Barrueco and/or Giuliana Manzolido.

Modifications to the Large Investments Incentive Regime and new implementation rules

The following regulations were published on October 22, 2024:

- Decree 940/2024 (“Decree 940”), which amends Decree 749/2024 (“Regulatory Decree”); and

- Resolution 1074/2024 of the Ministry of Economy (“Resolution 1074”), which approves the “Procedures for the Implementation of the Large Investments Incentive Regime” (“RIGI”).

The RIGI was created by Law 27,742 (“Foundations Law”) and regulated by the Regulatory Decree (see our comments on these regulations here and here).

1. Decree 940

Decree 940 amends certain aspects of the Regulatory Decree, such as:

- Capital goods destined to the realization of a RIGI Project are added as goods to be imported by suppliers adhered to the RIGI.

- The Single Project Vehicle (the “SPV” or Vehículo de Proyecto Único) may request the voluntary withdrawal of the RIGI provided that it has not been notified of an infringement procedure with a final resolution.

- The Tax for an Inclusive and Solidary Argentina (for its Spanish acronym, “Impuesto PAIS”) is suspended for the purchase of foreign currency destined to the payment of imports of capital goods made by the SPVs adhered to the RIGI.

2. Resolution 1074

Resolution 1074 establishes five procedures to adhere to the RIGI through the Trámites A Distancia (“TAD”) platform:

- Adhesion procedure for SPVs.

- Adhesion procedure for Strategic Long-Term Export Projects (“SLEP”).

- Adhesion procedure for the Expansion of Pre-existing Projects.

- Adhesion procedure for local suppliers; and

- Procedure to request a voluntary withdrawal of the RIGI.

3. Term for the resolution of applications

The term for the Ministry of Economy to approve or reject an application of adhesion or cancellation is forty-five (45) business days. This term may be suspended if additional information is required from other agencies or from the applicant.

In case of rejection, the applicant may submit a new application up to two additional times in the same calendar year.

4. Adhesion procedure

The adhesion procedure includes the following stages:

- Generation of an electronic docket with the Ministry of Economy.

- Preliminary analysis of the feasibility of the Project.

- Intervention of the Central Bank of Argentina and the Antitrust Agency, if necessary, which will temporarily suspend the procedure.

- Recommendation of the Evaluation Committee for the approval or rejection of the adhesion.

- Issuance of the Certificate of Adhesion to the RIGI for the approved Projects, allowing the SPVs to access the benefits and incentives.

5. Voluntary withdrawal

SPVs may withdrawal from the RIGI through the submission of a report explaining the reasons for their decision through the TAD platform.

***

For additional information, please contact Nicolás Eliaschev, Javier Constanzó, Daiana Perrone, Milagros Piñeiro, Victoria Barrueco and/or Giuliana Manzolido.

The Government of Argentina releases the implementation rules of the RIGI

On August 23, 2024, the Government of Argentina published Decree 749/2024 (“Decree 749”) which contains the implementation rules of the recent large-investment regime bill approved by Law 27,742 (for its Spanish acronym, “RIGI”) (for additional comments in connection with the RIGI and other aspects of the Foundations Law, please access here).

Further implementation rules from other governmental entities are to be published no later than 30 days following the publication of Decree 749.

The key takeaways of Decree 749 are summarized below:

1. Eligible Sole Purpose Vehicles

Existing sole Purpose Investment Vehicles (“SPVs”) may adhere to the RIGI. These include corporations (sociedades anónimas), sole proprietorships (sociedades anónimas unipersonales), Limited Liability Companies (sociedades de responsabilidad limitada), branches (sucursales), and joint ventures (uniones transitorias).

2. Minimum amount of investment

The Minimum Investment Amount (the “Minimum Amount”) remains at two hundred million United States dollars (US$ 200,000,000) (net of VAT) for most of the RIGI sectors, including Preexisting Projects subject to an Expansion (as such terms are defined below).

As to oil and gas transportation and storage, the Minimum Amount is set at three hundred million United States dollars (US$ 300,000,000). For offshore oil and gas exploration and production, and gas exports, the amount is set at six hundred million United States dollars (USD 600,000,000).

Finally, for Strategic Long-Term Export Projects (“SLEP”) the Minimum Amount is raised from one billion united states dollars (US$ 1,000,000,000) to two billion United States dollars (US$ 2,000,000,000).

3. Expansion of Preexisting Projects

Decree 749 defines an “Expansion” as the group of investments in qualifying assets that will result in the increase of the productive capacity of a project adhered to the RIGI, or a Preexisting Project (not adhered to the RIGI).

In this way, Preexisting Projects that comply with the requirements set by the RIGI, e.g., the Minimum Amount, may be eligible to adhere to the RIGI, but the benefits provided by the RIGI will solely apply to the Expansion (i.e., not to the Preexisting Project).

4. Qualifying Assets

Investments made before to the enactment of the RIGI in qualifying assets (including, in this definition, mining, oil & gas concessions, real estate, etc.) are not eligible for purposes of the Minimum Investment Amount, as Decree 749 further clarifies that only those made following the approval of the RIGI may be considered as Qualifying Assets.

5. Essential services

Decree 749 states that essential services, accountable up to 20% of the Minimum Amount, are defined as those without the RIGI project could not have been executed. Approval from the Enforcement Authority is required. Services provided by affiliates are excluded.

6. Strategic Long-Term Export Projects

To be considered as a SLEP project, Decree 749 further indicates that the following criteria must be met (apart from those provided in Decree 749 and in the RIGI):

- The SLEP will result in the international positioning of Argentina as a new long-term supplier in the global market.

- Each stage of the project shall involve a minimum investment amount of one billion United States Dollars (US$ 1,000,000,000).

- 20% of two billion United States Dollars shall be investment in the first and second year of the SLEP’s term.

- The components associated to the SLEP shall be interconnected, within a maximum radius of 200 km, provided that such radius shall not apply if the components are located at a greater distance but are physically integrated.

7. Tax and Customs Incentives

7.1. Income Tax

7.1.1. Income Tax Rate

The Decree 749 stipulates that the benefit of the 25% rate established by Section 183 of the Foundations Law will apply over net income subject to tax derived from SPVs’ activity, as of the SPVs’ adherence to the RIGI.

7.1.2. Special Amortization Regime

SPVS may choose to apply the amortization regime foreseen in the Income Tax Law or the accelerated amortization mechanism specifically foreseen by Section 183 of the Foundations Law. The Decree 749 specifies that in case the SPV opts for the latter, it shall be applied to all assets, of the SPV, and the assets must remain in the SPVs’ possession until the end of its activity or their lifespan, whichever occurs earlier. If this requirement is not met, the SPVs must reinstate the amortization previously deducted in its tax balance, considering it as taxable income and applicable interests shall accrue. Once the option is exercised, it must be reported to the Enforcement Authority and to the tax authority, and the assigned lifespan of the depreciable assets must be reported annually.

7.1.3. Transfer of Tax losses

Tax losses incurred by the SPVs can be transferred to third parties under the conditions specified by Section 183 of the Foundations Law. Decree 749 states that such third will be able to apply the assigned tax losses in the fiscal period in which they are assigned, even if this occurs after the end of that period (but before the due date for filing the Income tax return). Further, tax losses can be carried forward for 5 years.

Transferred losses will be considered general losses of Argentine source for the recipient.

The transfer is subject to approval from AFIP, which must issue a resolution within 45 business days.

If the AFIP rejects the transfer for formal reasons, the taxpayer may amend the inconsistencies, and AFIP must thereafter issue a new resolution within the following 10 business days. The third subject will be exempt from any liability if AFIP challenges the transferred loss, and the claim will be directed to the original SPV that generated it (except in cases where the SPV qualifies as a sole purpose branch, and the deduction of tax losses has been done by the parent company).

7.1.4. Dividends

Dividends will be subject to tax at a 7% rate if distributed to individuals or undivided estates. Decree 749 provides that after 7 years from the end of the tax period of SPVs’ adherence to the RIGI, a reduced tax rate of 3.5% will apply, as it is specified by Section 185 of the Foundations Law, regardless of the income origin.

7.1.5. Payments from Strategic Long-term Export Projects to foreign beneficiaries

30% of the amounts paid will be presumed as net income (unless a more favorable treatment or exemption under current regulations applies) and the withholding tax must be applied.

7.1.6. Transactions between affiliates

Transactions or operations that an SPV performs with affiliates (either located within the country or abroad) will be subject to the Transfer Pricing rules established by the Income Tax Law.

The transactions or operations that an SPV carries out with their related parties located in the country and abroad will be subject to the Income Tax Law’s rules.

Conversely, with regards to entities residing in Argentina, they will be considered as affiliates in case that the following requirements, established by the Decree 749, are met:

- A subject holds all or most of the stock capital of another.

- Two or more subjects have a common entity holding all or most of their stock capital.

- A subject holds the necessary votes to form the corporate will or prevail in the shareholders' or partners' assembly of another subject.

- The members of a joint venture, or any other associative agreements or the entity that created sole purpose branches, or the foreign companies’ branches and resident subjects in Argentina are related as per the points above.

- There are agreements, circumstances, or situations granting the direction to a subject, whose participation in the stock capital is minor.

The AFIP must amend the Transfer Pricing regime foreseen by the Income Tax Law in order to make it applicable to transactions performed between SPVs and related parties which reside in Argentina.

Section 186 second paragraph of the Foundations Law states that to determine if the cost-sharing agreements signed between SPVS and their related parties are aligned with market practices between independent parties, the value of contributions or inputs made by each participant must be equivalent to what an independent company would accept under comparable circumstances. In this regard, Decree 749 stipulates that:

- A subject is considered to be a participant in the agreement if they have a reasonable expectation of benefiting from the result of that agreement.

- Contributions and expected benefits should be valued as if they had occurred between independent parties.

- This contributions valuation should be made without considering the benefits obtained within the RIGI framework.

- In specific cases, the AFIP may determine the correct valuation of the participations and benefits attributable to each participant and may also create an information regime over the operations of SPVs.

7.2. Value-added Tax (“VAT”)

The amount of VAT invoiced to SPVs for the purchase of fixed assets or infrastructure investments and/or necessary services for their development and construction, or the VAT for definitive imports, will be applied to a Tax Credit Certificate, without requiring the AFIP’s authorization.

The SPVs must report to the AFIP the certificates issued on a monthly basis, and, if the AFIP detects inconsistencies, VAT must be paid along with its applicable interests and fines, and it will be computable by SPVs as a VAT credit against VAT debits in the following period.

7.3. Tax Treatment of Joint Ventures or other associative contracts

Decree 749 states that these subjects will be able to adhere to the RIGI as SPVs if they are formed by independent companies that are duly registered in the relevant Public Registry and whose economic activity is orientated to third parties (e.g., projected to market).

7.4. Imports

7.4.1. Exemptions

Section 109 of the Foundations Law establishes that Imports of capital goods, spare parts, components, among others, carried out by SPVs will be exempted from import duties, certain fees (including destination verification), and any regime of collection, payments in advance or withholding of national and/or local taxes.

Decree 749 specifies that exemptions will apply to imports directly related to the approved investment plan and, for that purpose, at the time of approving the SPVs’ adherence to the RIGI, the following information must be provided to the Enforcement Authority:

- Details of the goods for which the incentive is requested.

- Identification of the adhering SPVs and the respective RIGI project to which the goods will be allocated.

- An affidavit certifying that the goods will be allocated to the RIGI project.

- Additionally, a guarantee must be posted as provided in Section 182 of the Foundations Law.

The goods will be subject to destination verification and must be allocated to the RIGI project until the end of the goods’ lifespan, the project or SPVS’ termination, the re-exportation of such goods, the payment of taxes that should have been paid if the benefit had not been granted, and/or the resolution of the Enforcement Authority.

The SPVs cannot change the declared destination of the goods, and they may only be transferred to another SPVs which has previously adhered to the RIGI, with the prior authorization of the AFIP.

7.5. Tax Treatment of Sole Purpose Branches

The taxpayer who creates the sole purpose branch may opt for:

- Transfer tax benefits proportionally to the value of the net worth transferred to the branch, as transferable losses of Income Tax and VAT balances. In this case, there are two alternatives:

- Allocate tax credits proportionally to the net worth transferred.

- Transfer tax credits directly obtained from the purchase or manufacture of the transferred asset.

- Transfer the assets, which will keep the same value that they had for the entity who creates the sole purpose branch, without transferring tax benefits.

7.6. Tax and Customs Stability

Section 201 of the Foundations Law established the tax and customs stability for SPVs, regarding the incentives mentioned above, which cannot be affected by the repeal of existing regulations or the creation of a more burdensome or restrictive new law. Additionally, the Decree stipulates that stability will apply to taxes, tax rates, and contributions payable by SPVs, as well as to rights, fees, or other charges on imports or exports. The SPVs may oppose the imposition of additional taxes or higher tax rates than those previously established, and also have the right to benefit from any elimination or exemption of taxes of the general tax regime, as well as from a possible reduction in tax rates.

Consequently, SPVs adhered to the RIGI will have the right, for a period of 30 years from the date of adherence, to pay exclusively:

- Taxes with the incentives offered by the RIGI; and

- Taxes not covered by the RIGI that were in effect at the time of their adherence, until they are eliminated from the general tax regime.

7.7. Tax for an Inclusive and Solidarity Argentina

The Decree establishes the suspension of the payment of this tax (as established by Section 35 of Law No. 27.541, subsection a), which applies to the purchase of foreign notes and currencies and other currency exchange transactions made by Argentine residents for the import of goods which are subject to the incentives mentioned in Section 190 of the Foundations Law.

8. Foreign Exchange Incentives

8.1. Collections from exports of goods and Start-Up Date

According to Section 198 of the Foundations Law, collections from exports of goods made by the SPV are exempted from the obligation to enter and settle foreign currency by a percentage equivalent to 20%, 40%, and 100% starting from the second, third, and fourth year, respectively, counted from the “Start-Up Date” of the SPV.

Decree 749 defines Start-Up Date as the date falling on the earlier of: (a) first export of the RIGI project; or (b) 40% of the Minimum Amount in qualifying assets is completed (net of accountable investments that can only be counted up to 15% and 20% according to Sections 38 and 39 of Decree 749).

The Start-Up Date must be reported by the SPV to the Enforcement Authority, specifically detailing the manner in which one of the two conditions outlined in the first paragraph has been fulfilled (e.g., the date of the first export, disbursement, the amount and eligible asset to which it was applied, etc.). This information will be forwarded by the Enforcement Authority to the Central Bank of Argentina (“BCRA”)

8.2. Incentive Percentage

Decree 749 also clarifies that the percentages indicated in the previous point will be calculated based on the amount received according to the agreed sales terms of the exported goods, shipped after the period corresponding to the Start-Up Date has elapsed.

8.3. Export Financing

Decree 749 provides that the incentives set forth for the export of goods (i.e., the possibility of not settling collections up to certain percentages) will be applicable to advances, pre-financing, and post-financing of exports, to the same extent that the incentive applies to the financed export.

8.4. Local Financing

Decree 749 clarifies that, for the purposes of the foreign exchange incentives under the RIGI, local financings in foreign currency shall include financial indebtedness with local financial institutions, issuance of securities in the local market, or promissory notes and other instruments approved by the BCRA.

8.5. Prepayment of Debt and Absence of Minimum Stay Period

Decree 749 establishes that access to the foreign exchange market by the SPV for the repayment of the principal of financial indebtedness with foreign creditors can occur at any time before the due date of the service, provided that such financing has been entered and settled through the foreign exchange market.

In the case of direct investments by non-residents, the SPV may access the foreign exchange market for the repatriation of the investment at any time, provided that the investment has been entered and settled, without the need to comply with any minimum stay period.

8.6. Limits for Accessing the Foreign Exchange Market

Decree 749 establishes that, as long as the provisions of the general foreign exchange market regime impose the obligation to enter and settle all or part of the proceeds from exports, the BCRA may require that the SPV only be allowed to access the foreign exchange market for any purpose to the extent that the total amount of foreign currency entered from abroad and settled in the foreign exchange market by the participating VPU is, at the time of each access, greater than or equal to the amount of foreign currency demanded by that date for the project, including the requested access.

It is also clarified that the above will not apply to the payment of interest on financial indebtedness and/or dividend payments.

8.7. Contributions in Kind and Commercial Debt

Investments by the SPV made through direct foreign investment contributions of capital goods in kind or the importation of capital goods financed by the supplier or another foreign creditor with direct disbursement to the supplier will receive the same benefits as those entered and settled, provided that such investments have been duly registered following the procedures established by the Enforcement Authority and/or the BCRA.

8.8. Partial Entry and Settlement

In cases where the SPV has partially entered through the foreign exchange market amounts corresponding to capital contributions or other direct investments, or loans or other financial indebtedness with foreign creditors, access to the foreign exchange market for the payment of profits, dividends, or interest to non-resident entities may not exceed the proportional part of the capital contributions or other direct investments, and the loans or other financial indebtedness with foreign creditors that have been entered and settled through the foreign exchange market.

8.9. Collections in Pesos by Foreign Creditors

Non-resident creditors of the SPV, including related parties, who have received pesos in Argentina as a result of a collection against the SPV due to a breach by the SPV (e.g., in the case of the enforcement of collateral), as well as guarantors of the SPVs obligations -including related parties- whose collateral is expressly established in the debt agreements for the payment of said granted collateral, will have access to the foreign exchange market for the repayment of principal and interest under the same terms and conditions that would have applied to the SPV.

8.10. Collateral for Foreign Creditors

Decree 749 establishes that the BCRA may: (i) approve mechanisms for accessing the foreign exchange market to allow the SPV to establish collateral in Argentina or abroad for the payment of principal and interest on foreign indebtedness that has been entered and settled through the foreign exchange market; and (ii) allow to accumulate collections from exports of goods and services in accounts within the country or abroad for the purpose of securing the repayment of such indebtedness, for example, onshore and offshore reserve accounts.

8.11. Impact on the Normal Development of the Project

Decree 749 sets forth that if a SPV adhering to the RIGI verifies that the normal development and execution of its project has been affected by actions or omissions of public bodies and/or private entities involved in administrative procedures related to compliance with the formal and/or substantive requirements and/or conditions established in the foreign exchange regulations, the SPV may notify the Enforcement Authority about the existence of such a situation with a detailed explanation of the case, providing any evidence in its possession, if any, and identifying the public bodies and/or private entities and their respective officials, agents, or employees involved, so that, if applicable, the Enforcement Authority can immediately take the necessary measures to restore the normal development and execution of the SPVs project adhering to the RIGI.

Such measures must be taken by the Enforcement Authority within five (5) business days of receiving the SPVs notification, including sending a notice to all parties identified by the SPV requesting explanations regarding the reported situation. This is notwithstanding any administrative, civil, and criminal consequences that may arise from the situation reported by the SPV.

8.12. Additional Regulations by the BCRA

Within 30 calendar days of the publication of the Decree 749, the BCRA must issue the necessary complementary regulations to enable, with respect to foreign exchange regulations, the effective use of the rights recognized under the RIGI.

The aforementioned regulations will also address cases of contributions of goods by foreign entities and the mechanisms for handling collaterals for local and foreign financing, including the application of the SPVs own exports, up to the amount of foreign currency that the SPV has entered and settled through the foreign exchange market in relation to the foreign indebtedness, plus its interest.

8.13. Accumulation of Benefits

With respect to foreign exchange incentives, the benefits provided under the RIGI in this matter cannot be accumulated with the incentives of other existing or future promotional regimes, including, but not limited to, the following: (i) Decree No. 929/13; (ii) Decree No. 234/21; (iii) Decree No. 892/20; (iv) Decree No. 277/22; (v) Decree No. 679/22; and (vi) Decree No. 28/23, or any regulations that may replace them in the future.

9. Procedure to adhere to the RIGI

The filing of the application must contain the documentation required by the Decree 749, and shall be submitted to the Enforcement Authority, signed by the legal representative and notarized. The Enforcement Authority must issue its decision on the adherence of the SPV to the RIGI within forty-five (45) business days. If the Enforcement Authority decides to request additional information to analyze the feasibility of the project or to call the legal representative to a hearing, this term shall be suspended.

Once this term has been resumed, the Enforcement Authority shall issue a decision within the remaining days of the established term, or within the following fifteen (15) business days, the longer of the two. The lack of pronouncement shall not be interpreted as an acceptance.

In case of rejection of the application, an adjusted filing may be submitted up to two (2) times during the same calendar year in which the notification of the first rejection was received.

10. New Registries

Decree 749 creates the “Registry of Sole Purpose Vehicles”, the “Registry of Strategic Long-Term Export Projects”, and the “Registry of Suppliers of the Incentive Regime for Large Investments”.

11. Enforcement Authority

The Ministry of Economy is designated as the Enforcement Authority of the RIGI.

12. Jurisdiction and arbitration

The SPV may establish, together with the Enforcement Authority, at the time of the filing, the forms, procedures and other requirements to be observed to communicate the existence of a dispute. This notice shall be made to the Enforcement Authority with a copy to the Attorney General’s Office.

Likewise, the Decree 749 introduces the concept of “Arbitration Contract”. The SPV adhered to the RIGI must state in writing its acceptance that both the SPV and its partners or shareholders will resolve disputes through the mechanisms set forth in the Foundations Law. Once the adherence has been accepted, the Arbitration Contract will enter come into force as of the date of the administrative act approving the adherence request to the RIGI.

Also, the filing shall provide that the calculation of the compensation shall contemplate consequential damages and loss of profit, as well as the impact on the economic and financial balance of the project.

Exceptionally, the Enforcement Authority may propose to the National Executive, with the express consent of the SPV, specific dispute resolution mechanisms for the project.

***

For additional information, please contact Nicolás Eliaschev, Javier Constanzó, Julieta De Ruggiero, Francisco Molina Portela, Gastón Miani, or Leonel Zanotto.

Foundations Law: Renegotiation of Public Contracts

- Scope: Public works and concession contracts entered prior to the new administration taking office may be subject to renegotiation and/or termination.

- Procedure: The procedure may be initiated by the National Government or by request of the contractor. The renegotiation and/or termination must be approved by the National Executive Power, with the prior intervention of the Office of the Attorney General (“Procuración del Tesoro de la Nación”).

- General provisions: the Ministry of Economy shall establish the financial or economic guidelines to determine the renegotiation or termination of the contracts within thirty (30) business days after the release of Decree 713.

- Renegotiation provisions:

- The contractor shall waive to any claim arising from, or in connection with, consequential damages, loss of profit, unproductive expenses and possible economic damages of a similar nature, derived from the decrease in the rate of execution or suspension of the work or service due to an emergency situation. The contractor shall also waive any administrative and/or judicial claim in connection thereof.

- The contractor shall receive no compensation for the loss of profits for the works, goods or services which may be carved-out by the contract amendment.

- The renegotiation agreement shall establish the terms of payment of the amounts due to the contractor, if applicable.

- The rights and obligations of the parties arising from the renegotiation agreement shall guarantee the economic and financial balance of the contract.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Regulation of Public Work Concessions, Infrastructure and Services

- Tenor of the concession: Concessions may be for a fixed or variable tenor, based on the required investment, operation and maintenance costs, debt services, among other factors.

- Enforcement Authority: Ministry of Economy.

- Public Services: Public service concessions or licenses will continue to be ruled by their regulatory frameworks, notwithstanding the application of this regime mutatis mutandis.

- Selection process: Concessions shall be awarded following a call for bids, locally and/or internationally.

- Budget earmarks: Budget earmarks are required, if government funds are required for the concession.

- Amendments to the Concession Contract – economic and financial balance: Unilateral modifications to the Concession Contract made by the grantor related to the execution of the project must be compensated to the concessionaire to maintain the economic and financial balance of the concession. Likewise, the renegotiation is allowed, having to prove, by means of technical reports, the convenience for the public interest and the due legal, economic and financial analysis of the execution of the contract to be renegotiated. The renegotiation shall be carried out within twelve (12) months from the date of economic and financial imbalance and may be extended by agreement of the parties.

- Unilateral termination of the contract: The unilateral termination of the contract for reasons of public interest must be declared by the National Executive Power, with the prior intervention of the Ministry of Economy.

- Dispute settlement: Disputes shall be resolved, primarily, through a technical panel. Arbitration is allowed as well.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Private Initiative Regime

- Scope: The newly enacted Private Initiative Regime shall apply to public work contracts, public works, services and infrastructure concessions and PPP contracts.

- Enforcement authority: Ministry of Economy.

- Submission of Private Initiatives: Initiatives may be submitted (a) following a call for bids for projects considered to be of public interest; or (b) with no call for bids, in which case the promoter of the private initiative (the “Promoter”) shall provide substantiated reasons for the private initiative to be deemed as of public interest.

- Private Initiatives Information: The private initiatives shall detail the following information:

- Technical and financial background of the Promoter.

- Description of the project.

- Location, area of interest and related benefits.

- Estimated demand and associated annual growth rate.

- Analysis of the relevant legal aspects considering, among other factors, its area characteristics, implementation zone, and areas of interest.

- If applicable, a description of the works to be performed and/or services to be provided, with their technical analysis.

- Analysis of the technical, economic, and financial feasibility.

- Estimated CAPEX and OPEX.

- Analysis of the economic conditions associated to the contract, such as fees and tenor of the concession.

- Financing.

- Description of the most material risk factors related to the Private Initiative.

- Environmental impact studies.

The Privative Initiative shall be backstopped by a guarantee, in the form of an insurance bond or letter of credit, in a guaranteed amount equal to 0.5% of the estimated investment; provided, however, that this guarantee may not be required if the Promoter accredits that the guaranteed amount has been incurred in the preparation of the private initiative.

- Filing of the Private Initiative – Public Interest Declaration: The Enforcement Authority is enabled to request additional information or documentation, and shall have a term of sixty (60) days, extendable for the same term according to the complexity of the project, to prepare a non-binding report on the public interest and the eligibility of the proposal, considering its technical, economic and financial feasibility. If the Enforcement Authority considers that the proposal is as of public interest, it will submit the non-binding report to the National Executive Power, who will decide whether to grant such qualification or not, within a term of ninety (90) days, extendable for the same term according to the complexity of the project. If the initiative is rejected, the project Promoter will not be entitled to any compensation.

- Call for Bids: the call for bids shall be done within sixty (60) days following the declaration of public interest.

- Promoter’s Rights:

- The Promoter’s bid shall have priority with respect to other offers if the difference between each offer’s price is no greater than ten percent (10%). Tied parties shall have the right to improve their offers if the offered price’s difference is between ten (10%) and fifteen percent (15%).

- If the Promoter is not selected as the preferred bidder, the Promoter shall have the right to be reimbursed for the direct costs and expenses from the preferred bidder (such reimbursement will not exceed 1% of the bid, increasable to 3%).

- Assignment of rights to the private initiative is allowed for the benefit of the Promoter.

- Abrogation of Decree 966/2005: the prior Private Initiative Regime approved by Decree 966/2005 is abrogated.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Regulation of Foundations Law: Government reorganization and Sale of state-owned companies

On August 5, 2024, the Government released Decree 695/2024 (the “Decree 695”) that regulates Title II “State Reform” of Law 27,742 “Foundations Law” (“Ley de Bases y Puntos de Partida para la Libertad de los Argentinos”).

A summary of the most relevant aspects on the regulations related to Government reorganization and Sale of state-owned companies are described below. Additional comments to the Foundations Law on these subjects are also available here and here.

1. Government reorganization

The Ministry of Economy shall propose to the National Executive Power the modification, transformation, unification, liquidation or dissolution of public trust funds in accordance with Section 5 a), b) and c) of Law 27,742 and other applicable provisions.

In addition, Decree 695 empowers the Ministry of Economy to issue complementary regulations to implement this procedure.

2. Sale of state-owned companies

2.1. Report

For the purposes of obtaining the National Executive Power’s authorization to proceed with the sale of state-owned companies, the Ministry or Secretary in control of the respective state-owned company (list that includes ENARSA, AYSA, Belgrano Cargas, Intercargo, Corredores Viales, among others) must submit to the National Executive Power a detailed report with a specific proposal of the most adequate procedure and modality for the sale of such any state owned company (the “Report”), after the intervention of the Agency for the Transformation of State-Owned Companies (Agencia de Transformación de Empresas del Estado).

2.2. Call for bids

Call for bids shall be published for, at least, seven (7) days, and the last publications shall be made, at least, thirty (30) days prior to the deadline for the submission of bids, according to the complexity of the procedure. Additionally, the call for bids must be published on the website of the enforcement authority responsible for the procedure.

For international call for bids, the call also must be published in at least one website that allows adequate access to foreign interested parties, for a term of three (3) days, at least forty-five (45) calendar days prior to the deadline for the submission of bids. The enforcement authority may also issue invitations to participate to all those human or legal persons, with national or foreign capital, that considers convenient.

2.3. Liquidation

In the case of sale of the above mentioned companies when the transfer of contracts under execution to the provinces is required, the Report shall also detail the amounts involved in any such contract, as well as any related agreements.

The company in liquidation, in cooperation with the Agency for the Administration of State Assets (Agencia de Administración de Bienes del Estado) must elaborate an inventory of its assets, including their valuation. If applicable, a priority order for the sale of the assets must be defined.

2.4. Other provisions

Prior to the closing of contracts, the Office of the Attorney General (Procuración del Tesoro de la Nación) and the Agency for the Transformation of State-Owned Companies may make observations and/or suggestions. In that event, the enforcement authority shall perform the referred modifications, and submit a final report to the National Executive Power for its approval. Once the procedure is completed, the enforcement authority shall draft a final report to the General Auditor Office.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.

Foundations Law: Labor Reform

1. Promotion of registered employment

Employers may regularize, within 90 days as of the regulation of the Foundations Law, the labor relations that are not registered or were registered in a deficient or partial manner (lower remuneration or date of entry after the real one).

The regulation of the law will precisely define the effects of this regularization, which in principle would include: (i) the extinction of the criminal action in process and the remission of fines for infractions; (ii) the removal of the employer from the registry with labor sanctions (“REPSAL”); (iii) the remission of debts of withholdings and contributions (except health care regime) in no less than 70% of the total; including those that are in dispute in a court of law.

Workers whose contracts have been regularized within the framework of the law and its regulations, will be entitled to compute, only for the purposes of the payment of the Universal Basic Benefit ("PBU") and for Unemployment Benefit, up to 60 months of services with contributions, calculated on the amount of the minimum, vital and mobile salary.

2. Labor modernization

Under this heading, the Foundations Law produces a very significant labor reform over the Employment Contract Act (“ECA”) and other labor regulations; the most important guidelines of which are as follows:

2.1. Repeal of fines for irregular registration

The Foundations Law eliminates all provisions of the National Employment Law No. 24,013 which set fines for lack of registration or deficient registration of the employment relationship. Law No. 25,323, which imposed fines for irregular registration (Section 1) and for failure to pay severance payments for dismissal without cause (Section 2) are also repealed by the Foundations Law.

2.2. Elimination of fines for failure to deliver work certificates

Through the repeal of Sections 43 to 48 of Law No. 25,345, the fines related to the failure to deliver the certificates of services and remunerations (Section 80 ECA) and for failure to pay the contributions withheld from the worker (Section 132 bis ECA) are eliminated.

2.3. Registration of the employment contract

There will be a new mechanism for the registration of the employment relationship, to be defined by the regulations, which will be simple and electronic. There will also be a simple mechanism for the issuance of salary slips and a unified contribution will be provided for companies with up to 12 workers.

2.4. Contractors and intermediaries

The law sets out the validity of the registration made by the original employer in relationships with contractors and staffing agencies. In the same sense, due to the amendment of Section 29 of the ECA, it is established that workers hired by third parties to be assigned to companies will be considered direct employees of the company which register the relationship, thus eliminating the risk of irregular registration of workers assigned to companies by third party contractors.

2.5. Deficient Registration

The worker may denounce the lack or partial registration of the employment relationship before the AFIP, through the electronic means that the authority will offer for such purposes. If such deficiency is established by the Court, the Judge will report the AFIP, which will determine the relevant social security debts. The corresponding debt will consider the contributions paid by the independent contractor.

2.6. Scope of application of the ECA

Service and agency contracts (among others) regulated by the National Civil and Commercial Code are excluded from the scope of application of the ECA.

2.7. Presumption of employment contract. Civil contracts

Professional services or trades that foreseen the issuance of official invoices by the provider do not fall under the presumption of the existence of an employment contract when the services are rendered by individuals. This understanding extends its effect to Social Security obligations.

2.8. Trial period

The trial period (Section 92 bis ECA) is of 6 months. This period may be extended by collective agreements to 8 months in companies with 6 to 100 workers, and up to 12 months in companies with a payroll of no more than 5 workers. These provisions will also apply to the national agricultural labor regime.

2.9. Pregnancy protection

The prohibition for pregnant women to work during the 45 days before and after childbirth is maintained, although as a result of the reform the employee is granted the option to reduce the pre-birth leave to 10 days, accumulating the remaining period to the postpartum period.

2.10. Just cause for dismissal

The law amends Section 242 of the ECA, expressly including as causes for dismissal, the following: (i) active participation in blockades or takeovers of the establishment; (ii) when as a result of the participation in strikes, (a) the freedom to work of those who do not participate in the strike is affected; (b) the entry of persons or things to the establishment is obstructed; (c) damage is caused to persons or assets of the company or third parties. Before dismissal because of these non-compliances, the employer must formally request the worker to abandon his attitude. This request is not necessary in the case of damage to persons or things.

2.11. Special compensation for discriminatory dismissal

Judges may increase the severance compensation between 50% and 100% (depending on the seriousness of the discriminatory act) in cases where the employee proves before Court that his/her dismissal was motivated by reasons of ethnicity, race, nationality, sex, gender identity, sexual orientation, religion, ideology or political or union opinion. Despite the discrimination scenario, the employee will not have the right to claim reinstatement.

2.12. Severance fund

Within the framework of a collective bargaining agreement, the parties may replace the current severance payment scheme with a "severance fund ". Its characteristics will be defined by the regulations. On the other hand, employers may choose to contract a private capitalization system (or self-insure) to cover the cost of the severance indemnification provided by the ECA or for the payment of a bonus agreed within the framework of mutual termination agreement.

2.13. Independent worker with collaborators

The Foundations Law incorporates a new category of self-employed workers, providing that an autonomous worker may work with up to 3 self-employed workers to carry out a productive undertaking, under a special regime to be regulated by the National Executive Power. There will be no employment relationship between those parties, unless in the reality of the relationship the notes of subordination that characterize any relationship of dependency are visualized. Anyway, as per the conditions to be defined by regulations, these workers will be included under the Social Security regimen, Health Care, and the Labor Hazards Law.

***

For additional information, please contact Federico Basile.

Law on Palliative and Relevant Tax Measures

On June 28th, 2024, the National Chamber of Deputies finally passed the Law on "Palliative and Relevant Tax Measures" (the "Tax Measures"), rejecting the amendments introduced by the National Senate on Income Tax (for employees) and Personal Assets Tax.

Below, we summarize the most relevant aspects of the Tax Measures:

Exceptional Regularization Regime for Tax, Customs, and Social Security Obligations (“moratorium”)

- Included obligations: the moratorium applies to tax, customs, and social security obligations (with some exclusions) due by March 31, 2024, inclusive, and for infringements committed up to that date, whether related to those obligations or not.

- Compensatory and punitive interests forgiveness: the moratorium establishes the following scheme for interests forgiveness: a) 70% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments, and the adherence to the moratorium takes place within the first 30 calendar days from the issuance of the regulation by the Tax Authorities (hereinafter, the “AFIP”, as per its acronym in Spanish); b) 60% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 31st to the 60th calendar day; c) 50% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 61st calendar day to the 90th calendar day; d) 40% of forgiveness if total debt is regularized through a payment plan and the adherence to the moratorium takes place within the first 90 calendar days; e) 20% of forgiveness if the total debt is regularized through a payment plan and the adherence to the moratorium takes place after the 91st calendar day.

- Financing: for cases d) and e) mentioned above, it is established that: (i) individuals must make a prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 60 monthly installments; (ii) Micro and Small Enterprises must make a prepayment of 15% of the debt and they are allowed to pay the remaining amount in up to 84 monthly installments; (iii) Medium Enterprises must make prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 48 monthly installments; (iv) other taxpayers must make a prepayment of 25% of the debt and they are allowed to pay the remaining amount in up to 36 monthly installments. In all cases, future regulations will set a financing interest, which will be calculated according to the rate established by the Banco de la Nación Argentina for commercial discounts.

- Other benefits: the adherence to moratorium implies the forgiveness of 100% of fines and the extinction of criminal actions.

Asset Regularization Regime (“Tax amnesty”)

- Subjects: (i) individuals, undivided estates, and companies that, as of December 31th, 2023, are deemed Argentine tax residents, whether or not they are registered as taxpayers before AFIP; (ii) individuals who were Argentine tax residents before December 31th, 2023, but have lost such status by that date. If latter adhere to the Tax amnesty, they will be deemed Argentine residents as of January 1st, 2024.

- Adherence period: the referred subjects can adhere to the Tax amnesty up to April 30th, 2025. The National Executive Branch may extend this period until July 31st, 2025.

- Included Assets: assets located in the country and abroad, including national and foreign currency, movable and immovable property, securities and shares, credits and rights, cryptocurrencies (only as assets in the country) owned, possessed, hold, or custodied by the taxpayer as of December 31st, 2023.

- Special tax: the special tax rate will be 5%, 10%, or 15%, depending on the moment in which the tax return is filed, and the payment is made.

- Amnesty without special tax: subjects will be able to regularize up to USD 100,000 without any penalty. If the amount subject to amnesty exceeds USD 100,000, no penalty will apply if the funds remain in a special account until December 31st, 2025. Amounts deposited in the special account can be invested in certain financial instruments specified by the regulation.

- Benefits: (i) extinction of all civil or criminal actions derived from the non-compliance of obligations related to the regularized assets; (ii) tax and interest forgiveness; (iii) inapplicability of the unjustified wealth increase presumption.

Personal Assets Tax ("PAT")

Special PAT Prepayment Regime: Tax Measures include an optional and voluntary prepayment regime for PAT, which has the following characteristics:

- Subjects: (i) individuals and undivided estates that, as of December 31st, 2023, are deemed Argentine tax residents; (ii) individuals who were Argentine tax residents before December 31st, 2023, but lost such status by that date. If they adhere to this Regime, they will be deemed Argentine tax residents again.

- Adherence period: subject will be able to adhere to this regime up to July 31st, 2024. This period may be extended up to September 30th, 2024.

- Included tax periods: 2023 to 2027 (unified) or 2024 to 2027 (unified) in case of taxpayers that have adhered to the Tax amnesty.

- Calculation method: PAT tax base is determined by considering the taxpayer's assets as of December 31st, 2023 -with certain particularities- multiplied by 5.

- Tax rates: the following rates are applied: (i) individuals and undivided estates: 0.45%; (ii) taxpayers who have regularized assets under the Tax amnesty: 0.50%. Since tax period 2028, maximum tax rate will be 0,25%

- Initial payment: taxpayers adhered to this regime must make an initial prepayment of -at least- 75% of the total PAT determined according to the regime's rules.

- Benefits: (i) exclusion from the payment of PAT and any other wealth tax for the tax periods 2023 to 2027 (or 2024 to 2027, as the case may be); and (ii) tax stability on those taxes up to 2038.

PAT Law:

- Certain modifications are established for the tax period 2023.

- The PAT non-taxable minimum is modified: ARS 100,000,000 (or ARS 350,000,000 for real estate that qualifies as only residence).

- The Tax measures include the unification of PAT rates for assets located in the country and assets located abroad as follows:

- Tax period 2023: from 0.50% to 1.50%;

- Tax period 2024: from 0.50% to 1.25%;

- Tax period 2025: from 0.50% to 1%;

- Tax period 2026: from 0.50% to 0.75%;

- Tax period 2027: a single rate of 0.25%.

- The Tax measures include benefits for compliant taxpayers:

- To qualify as a compliant taxpayer, the taxpayer (i) must not have regularized assets under the Tax amnesty; and (ii) must have submitted the PAT returns related to tax periods 2020 to 2022, inclusive, in a timely and proper manner, and must have fully paid, before December 31st, 2023, the PAT due to the AFIP resulting from each of those tax returns.

- Compliant taxpayers will have a 0.50% reduction in the PAT rates for tax periods 2023 to 2025.

Income Tax ("IT")

- The Tax measures repealed the “cedular IT” previously applied to employees, which established a special and unique deduction equivalent to 180 annual minimum salaries for IT determination.

- In replacement, it is created a new regime to determine employees’ IT.

- This new regime repeals certain exemptions, deductions, and benefits previously applicable to employees.

- Certain personal deductions are reinstated.

- Non-taxable minimums, scales, and personal deduction amounts are updated.

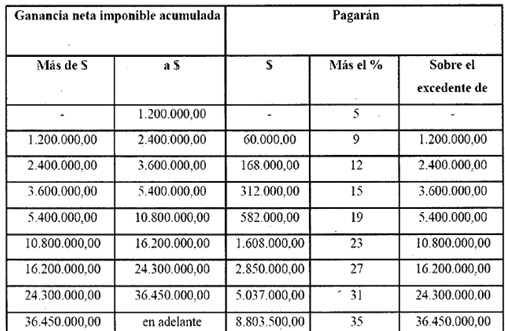

- The following scale is established for employees’ IT determination:

- From 2025, scales will be adjusted for inflation every semester (in January and July of each year) based on the CPI (Consumer Price Index).

- An exceptional adjustment for inflation will take place in September 2024, regarding months June to August. Therefore, the amounts corresponding to the first half of the current year will not be adjusted.

- The National Executive Power is authorized to exceptionally increase deductions during 2024.

-

Other modifications

- The billing caps of the Simplified Regime for Small Taxpayers were updated. The National Executive Power is authorized to increase those caps during 2024.

- The Real Estate Transfer Tax (“ITI”) was repealed.

- A tax transparency regime for consumers was created.

-

***

For additional information, please contact Gastón Miani or Leonel Zanotto.

Foundations Law: Electric Energy

The National Executive Power is entrusted, for a term of one (1) year, to make amends to the electric energy regulatory framework, namely composed by Laws No. 15,336 and No. 24,065, in order to guarantee, among others, free international trade of electric energy; free commercialization and expansion of the electric energy markets; the adjustment of the fees of the energy system based on the real costs of the supply, to cover investment needs and guarantee the continuous and regular provision of public services; and the development of electric energy transportation infrastructure.

Common regulations on electric energy and natural gas chapters

Appeals and objections to sanctions

Acts and sanctions issued by the highest authority of the regulatory body may be challenged without the need to file an appeal, directly before the National Court of Appeals for Federal Administrative Matters.

Unification of regulatory bodies

Foundations law unifies the electricity and gas regulatory bodies under a single entity, the “Ente Regulador del Gas y la Electricidad”.

***

For additional information, please contact Nicolás Eliaschev and/or Javier Constanzó.