On June 28th, 2024, the National Chamber of Deputies finally passed the Law on “Palliative and Relevant Tax Measures” (the “Tax Measures“), rejecting the amendments introduced by the National Senate on Income Tax (for employees) and Personal Assets Tax.

Below, we summarize the most relevant aspects of the Tax Measures:

Exceptional Regularization Regime for Tax, Customs, and Social Security Obligations (“moratorium”)

- Included obligations: the moratorium applies to tax, customs, and social security obligations (with some exclusions) due by March 31, 2024, inclusive, and for infringements committed up to that date, whether related to those obligations or not.

- Compensatory and punitive interests forgiveness: the moratorium establishes the following scheme for interests forgiveness: a) 70% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments, and the adherence to the moratorium takes place within the first 30 calendar days from the issuance of the regulation by the Tax Authorities (hereinafter, the “AFIP”, as per its acronym in Spanish); b) 60% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 31st to the 60th calendar day; c) 50% of forgiveness if the payment is made in cash or through a payment plan of up to 3 monthly installments and the adherence to the moratorium takes place from the 61st calendar day to the 90th calendar day; d) 40% of forgiveness if total debt is regularized through a payment plan and the adherence to the moratorium takes place within the first 90 calendar days; e) 20% of forgiveness if the total debt is regularized through a payment plan and the adherence to the moratorium takes place after the 91st calendar day.

- Financing: for cases d) and e) mentioned above, it is established that: (i) individuals must make a prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 60 monthly installments; (ii) Micro and Small Enterprises must make a prepayment of 15% of the debt and they are allowed to pay the remaining amount in up to 84 monthly installments; (iii) Medium Enterprises must make prepayment of 20% of the debt and they are allowed to pay the remaining amount in up to 48 monthly installments; (iv) other taxpayers must make a prepayment of 25% of the debt and they are allowed to pay the remaining amount in up to 36 monthly installments. In all cases, future regulations will set a financing interest, which will be calculated according to the rate established by the Banco de la Nación Argentina for commercial discounts.

- Other benefits: the adherence to moratorium implies the forgiveness of 100% of fines and the extinction of criminal actions.

Asset Regularization Regime (“Tax amnesty”)

- Subjects: (i) individuals, undivided estates, and companies that, as of December 31th, 2023, are deemed Argentine tax residents, whether or not they are registered as taxpayers before AFIP; (ii) individuals who were Argentine tax residents before December 31th, 2023, but have lost such status by that date. If latter adhere to the Tax amnesty, they will be deemed Argentine residents as of January 1st, 2024.

- Adherence period: the referred subjects can adhere to the Tax amnesty up to April 30th, 2025. The National Executive Branch may extend this period until July 31st, 2025.

- Included Assets: assets located in the country and abroad, including national and foreign currency, movable and immovable property, securities and shares, credits and rights, cryptocurrencies (only as assets in the country) owned, possessed, hold, or custodied by the taxpayer as of December 31st, 2023.

- Special tax: the special tax rate will be 5%, 10%, or 15%, depending on the moment in which the tax return is filed, and the payment is made.

- Amnesty without special tax: subjects will be able to regularize up to USD 100,000 without any penalty. If the amount subject to amnesty exceeds USD 100,000, no penalty will apply if the funds remain in a special account until December 31st, 2025. Amounts deposited in the special account can be invested in certain financial instruments specified by the regulation.

- Benefits: (i) extinction of all civil or criminal actions derived from the non-compliance of obligations related to the regularized assets; (ii) tax and interest forgiveness; (iii) inapplicability of the unjustified wealth increase presumption.

Personal Assets Tax (“PAT“)

Special PAT Prepayment Regime: Tax Measures include an optional and voluntary prepayment regime for PAT, which has the following characteristics:

- Subjects: (i) individuals and undivided estates that, as of December 31st, 2023, are deemed Argentine tax residents; (ii) individuals who were Argentine tax residents before December 31st, 2023, but lost such status by that date. If they adhere to this Regime, they will be deemed Argentine tax residents again.

- Adherence period: subject will be able to adhere to this regime up to July 31st, 2024. This period may be extended up to September 30th, 2024.

- Included tax periods: 2023 to 2027 (unified) or 2024 to 2027 (unified) in case of taxpayers that have adhered to the Tax amnesty.

- Calculation method: PAT tax base is determined by considering the taxpayer’s assets as of December 31st, 2023 -with certain particularities- multiplied by 5.

- Tax rates: the following rates are applied: (i) individuals and undivided estates: 0.45%; (ii) taxpayers who have regularized assets under the Tax amnesty: 0.50%. Since tax period 2028, maximum tax rate will be 0,25%

- Initial payment: taxpayers adhered to this regime must make an initial prepayment of -at least- 75% of the total PAT determined according to the regime’s rules.

- Benefits: (i) exclusion from the payment of PAT and any other wealth tax for the tax periods 2023 to 2027 (or 2024 to 2027, as the case may be); and (ii) tax stability on those taxes up to 2038.

PAT Law:

- Certain modifications are established for the tax period 2023.

- The PAT non-taxable minimum is modified: ARS 100,000,000 (or ARS 350,000,000 for real estate that qualifies as only residence).

- The Tax measures include the unification of PAT rates for assets located in the country and assets located abroad as follows:

- Tax period 2023: from 0.50% to 1.50%;

- Tax period 2024: from 0.50% to 1.25%;

- Tax period 2025: from 0.50% to 1%;

- Tax period 2026: from 0.50% to 0.75%;

- Tax period 2027: a single rate of 0.25%.

- The Tax measures include benefits for compliant taxpayers:

- To qualify as a compliant taxpayer, the taxpayer (i) must not have regularized assets under the Tax amnesty; and (ii) must have submitted the PAT returns related to tax periods 2020 to 2022, inclusive, in a timely and proper manner, and must have fully paid, before December 31st, 2023, the PAT due to the AFIP resulting from each of those tax returns.

- Compliant taxpayers will have a 0.50% reduction in the PAT rates for tax periods 2023 to 2025.

Income Tax (“IT”)

- The Tax measures repealed the “cedular IT” previously applied to employees, which established a special and unique deduction equivalent to 180 annual minimum salaries for IT determination.

- In replacement, it is created a new regime to determine employees’ IT.

- This new regime repeals certain exemptions, deductions, and benefits previously applicable to employees.

- Certain personal deductions are reinstated.

- Non-taxable minimums, scales, and personal deduction amounts are updated.

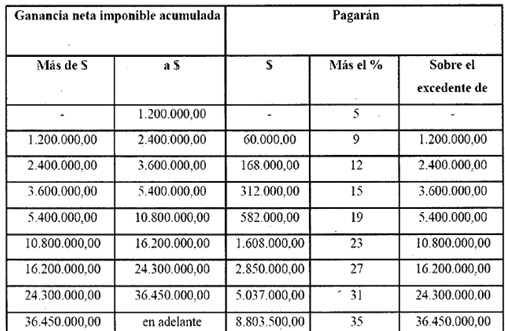

- The following scale is established for employees’ IT determination:

- From 2025, scales will be adjusted for inflation every semester (in January and July of each year) based on the CPI (Consumer Price Index).

- An exceptional adjustment for inflation will take place in September 2024, regarding months June to August. Therefore, the amounts corresponding to the first half of the current year will not be adjusted.

- The National Executive Power is authorized to exceptionally increase deductions during 2024.

-

Other modifications

- The billing caps of the Simplified Regime for Small Taxpayers were updated. The National Executive Power is authorized to increase those caps during 2024.

- The Real Estate Transfer Tax (“ITI”) was repealed.

- A tax transparency regime for consumers was created.

-

***

For additional information, please contact Gastón Miani or Leonel Zanotto.